Medicare Planning

What Is The Medicare Savings Program?

The Medicare Savings Program (MSP) is designed to help individuals with limited income pay for some of their Medicare expenses—but

Medicare Planning

“How Much Does My Medicare Cost Each Month?”

What Are People Asking? ● “Is Medicare free when I turn 65?” ● “Why do I have to pay for

Medicare Planning

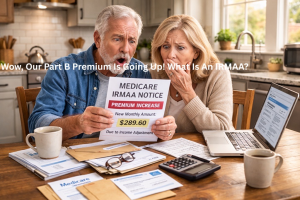

Why Is My Medicare Part B Premium Going Up And What’s An IRMAA?

What Are People Asking? ● “Why did my Medicare Part B premium go up?” ● “What is IRMAA and why

Medicare Planning

2026 Medicare costs

Key Takeaways Is Medicare Part A Free? Is My Income Used To Determine the Cost Of Part B? What About